Better Safety.

Better Risk.

Better Rates.

The workplace safety and training platform built for small businesses — and the insurance partners who serve them.

Smarter Risk delivers risk assessments, safety program building, and employee training in one complete solution.

A $150 value — no credit card required.

Everything small businesses need to prevent injuries and earn better insurance rates — trusted by insurance carriers and agents to extend risk control to their policyholders.

Everything you need to build a safer,

more insurable business.

All four work together — your assessment drives your program, your program drives your training,

and every improvement is tracked and documented. One platform, start to finish.

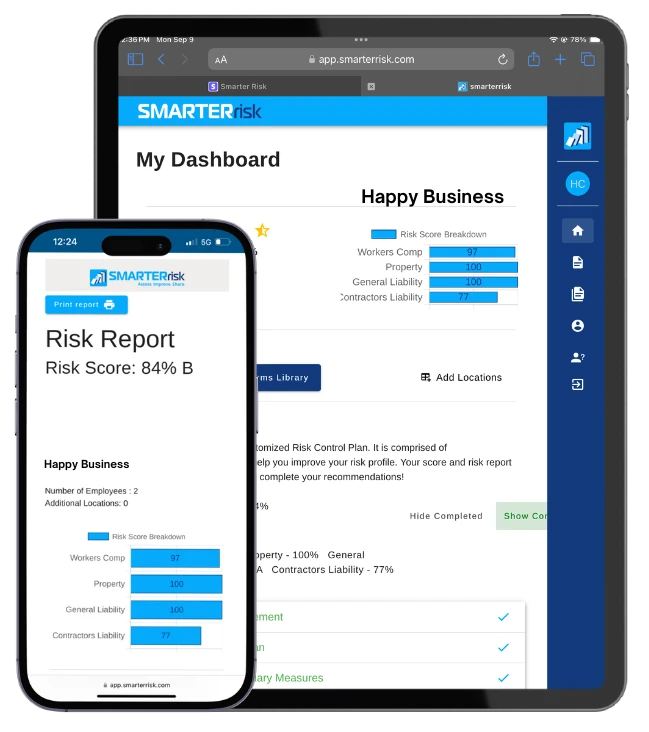

Risk Assessment — Done in 15 Minutes

Know exactly where you stand. Our AI assistant RISK-B guides you through a complete safety and risk assessment in just 15 minutes — identifying hazards, policy gaps, and training needs across your entire operation. The moment you finish, your personalized risk improvement plan is ready.

Safety Program Builder

Turn findings into action. Generate OSHA, NFPA, and ANSI-aligned safety programs in a few clicks — no $10,000 consultant, no months of drafting. Professional-grade programs, tailored to your business and ready to implement.

Online Employee Training

Get your team certified fast. SmarterRisk includes 50+ safety courses, unlimited seats, and a full built-in Training Director (LMS) — assign, track, and document training for your whole team, on any device, on their schedule. No per-user fees, no surprise charges.

150+ Safety Forms Library

Stop searching the web for the right form. SmarterRisk includes over 150 ready-to-use safety and compliance forms, included at no extra cost.

The numbers don't lie.

A 2011 Ohio Bureau of Workers' Compensation study found that businesses with structured safety programs saw dramatic improvements:

SmarterRisk helps small businesses replicate these outcomes — quickly and affordably.

Built for businesses where safety really matters.

SmarterRisk is designed for small businesses in the manual labor industries where workplace injuries are most costly — and most preventable. For example:

If your team works with tools, machines, hazardous materials, or in physically demanding conditions —

SmarterRisk was built for you.

Three steps to a safer,

more insurable business.

Assess

Start with a digital safety and risk assessment. In 15 minutes, RISK-B assists in identifying exactly what's exposing your business — and builds your action plan.

Improve

Close the gaps. Build safety programs, assign training to your team, and document controls with photo verification — your safety score updates in real time.

Share

Share verified improvements with your insurance partners. Documented, measurable risk profile improvements — the very thing insurers look at when determining rates.

Systemize safety so it works for you.

Trusted by small businesses and the insurance partners who protect them.

Learn how companies use SmarterRisk to build safer workplaces.

"SmarterRisk is an exceptional tool that has rapidly enhanced our risk management and safety capabilities. Without it, manual improvements would have been nearly impossible. Thanks to SmarterRisk, we not only knew exactly what to do but excelled when our insurance company conducted their risk assessment. We passed with flying colors."

— Scott Damer, COO, The Beamery LLC, Helmsburg, IN

"Using SmarterRisk transformed how I see my business and its potential risks. The app guided me through the safety assessment process, providing valuable insights into key improvements I could make. SmarterRisk is an indispensable tool for any business looking to improve safety and qualify for better insurance rates."

— Randy Claybrook, Owner, Bent Creek Lodge, Asheville, NC

Who We Serve

Built with your clients in mind.

SmarterRisk helps your small business policyholders do the work that reduces risk — documented assessments, real safety programs, trained employees. Better-prepared clients mean better outcomes at renewal, fewer claims, and stronger relationships.

Click the links below to see what our specific product can do for you.

Frequently Asked Questions

1. What is SmarterRisk?

SmarterRisk is workplace safety software that helps small businesses build safety programs, train employees, and document improvements — all in one platform. By turning workplace safety into an ongoing process instead of a one-time event, SmarterRisk reduces injuries, improves OSHA compliance, and helps lower workers' comp costs. Built specifically for small businesses in hands-on industries — contractors, shops, warehouses, manufacturing, restaurants, and hotels.

2. How long does it take to complete a safety assessment?

Our AI-assisted assessment takes just 15 minutes — not hours — to complete for your entire organization. The moment you finish, your custom risk improvement plan is generated instantly, showing you exactly what to focus on to improve workplace safety. You only need one assessment per organization. If you have multiple locations, you can create an assessment for each one, up to 10 on a single account.

3. Can I try SmarterRisk before committing?

Absolutely. Your safety assessment (single location) is free — a $150 value. See where your business stands, get a personalized risk improvement plan, and start building a safer workplace today. Get started now with no credit card required.

4. Are safety training materials included?

Yes. Our Intelligent Plan includes full access to Training Director, our complete Learning Management System with 50+ safety courses. Assign training, track completion, test knowledge, and generate compliance reports — all with unlimited seats at no additional cost. No per-user fees, no surprise charges — just complete training management for your entire team.

5. Will using SmarterRisk help lower my insurance premiums?

While we can't guarantee premium reductions, SmarterRisk helps you build, document, and maintain safety programs that insurers recognize — improving your overall risk profile and supporting better rates. Studies show that written safety programs reduce claims by 52%, lower claim costs by 80%, and decrease lost-time days by 87%. Want to estimate the potential savings? Try our Safety ROI Calculator to see the real financial impact of implementing effective safety programs.

6. Do I need safety experience to use SmarterRisk?

No safety expertise required. Our platform is designed for business owners and managers, not safety professionals. RISK-B, our built-in AI assistant, guides you through every step and can answer any questions about workplace safety. Safety programs are automatically formatted to meet OSHA, NFPA, and ANSI standards — professional-grade results without the expertise.

7. Can I share my assessment results with my insurance agent or carrier?

Yes! You can generate and share a comprehensive risk report with your insurance partners. Many agents and carriers use these reports for underwriting, renewal discussions, and proving your commitment to workplace safety — which can lead to better rates and terms.

8. What if I need help or have questions?

RISK-B, our built-in AI assistant, is available 24/7 to answer questions about workplace safety or using the platform. Our AI assistant provides instant, expert guidance whenever you need it.

9. Does SmarterRisk integrate with other systems?

SmarterRisk is 100% cloud-based and doesn't require integration with payroll, HR, or other software. This means you can start using it immediately without IT involvement. Everything you need — assessments, safety programs, training, and reporting — is in one simple platform.

Get in Touch

Have questions? Contact us below or fill out the form and we'll get back to you as soon as possible.